Moody's, the world is watching

My take at an answer to Rene Lipsch, Moody's Analyst in charge of rating Tesla

Dear Mr. Lipsch, dear Renier,

I’m truly obliged for your response to my request about considering Tesla for a rating upgrade over the next few months to Investment Grade.

Your point of view that ratings should include both qualitative and quantitative components is understandable. After all, quantitative yardsticks measure the past, whereas investment and lending decisions are made for the future. And with today’s global access to detailed financial information, compiling ratings solely on quantitative measures would make them instantly irrelevant.

We do agree Tesla deserves an investment-grade rating based on quantitative measures. So the question remains: do Tesla’s current qualitative measures so overwhelm their persistently excellent quantitative factors to justify the current low rating?

Please allow me to elaborate on some salient qualitative factors:

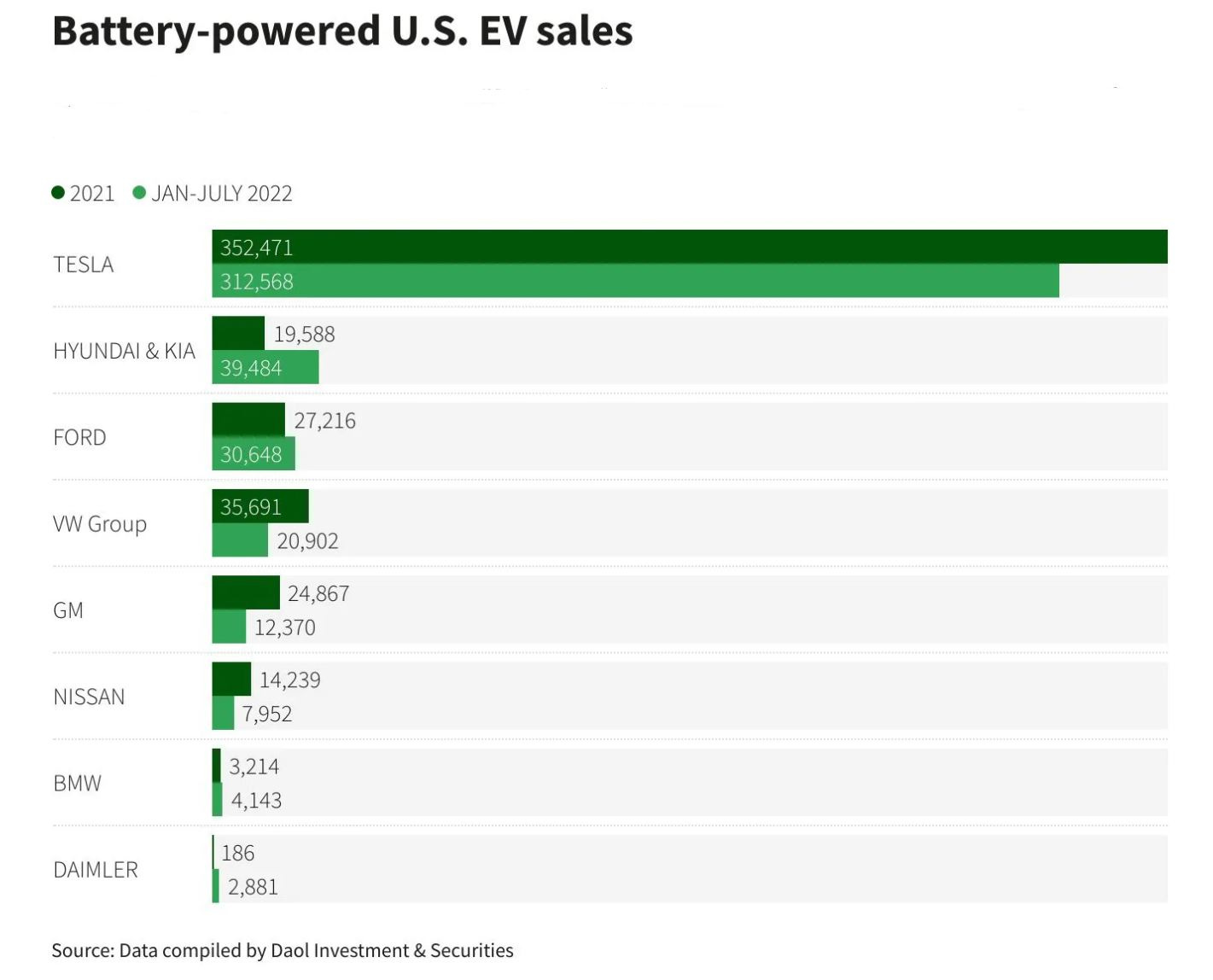

COVID caused global supply chain issues throughout automotive manufacturing and chip shortages were a particularly vexing concern. When Tesla could no longer source required chips, they demonstrated flexibility and engineering prowess by switching to available chips and writing code to transform available chips into functional equivalent chips. This was accomplished while concurrently growing revenue and profit on a pace equal to their pre-COVID guidance. From this qualitative perspective, which deserves an Investment Grade rating: an agile, resourceful automaker or top Investment Grade automakers struggling to adapt to global shortages?

In your response you mentioned 2017, the year in which the Model 3 was launched. This is not old for a car brand (Toyota Camry was launched in 1982, Ford F150 in 1975). Please remember, Tesla customers don’t buy stale cars, because Tesla constantly improves them. Customers receive a better car than it was at the time they happily ordered one, which as you are aware comes currently with months-long wait times. And this experience continues after the customer purchases the car, as regular over-the-air updates ensure the whole fleet of now more than 3 million cars operates on the latest software. From a qualitative point of view, would you like to experience an always updated car as a customer, and hence great resale value, or would you prefer to drive a model that gets stale after purchase? From an investment point of view, does a company that takes such great care of its customers should have its investment-grade rating dinged?

These constant improvements also help Tesla to keep their margins higher because cost savings are implemented every single day instead of being postponed until the next (cosmetic) upgrade in a few years. Automobile industry expert John McElroy in Wardsauto states “Tesla makes design changes on the fly. And it mainly makes those changes – this is a key point – to take cost out of its cars”. The great and ever improving financial numbers Tesla posts every quarter are a reflection of this manufacturing prowess indicated above. From a qualitative point of view, does that indicate that such a company is relatively likely to continue to post great financial results?

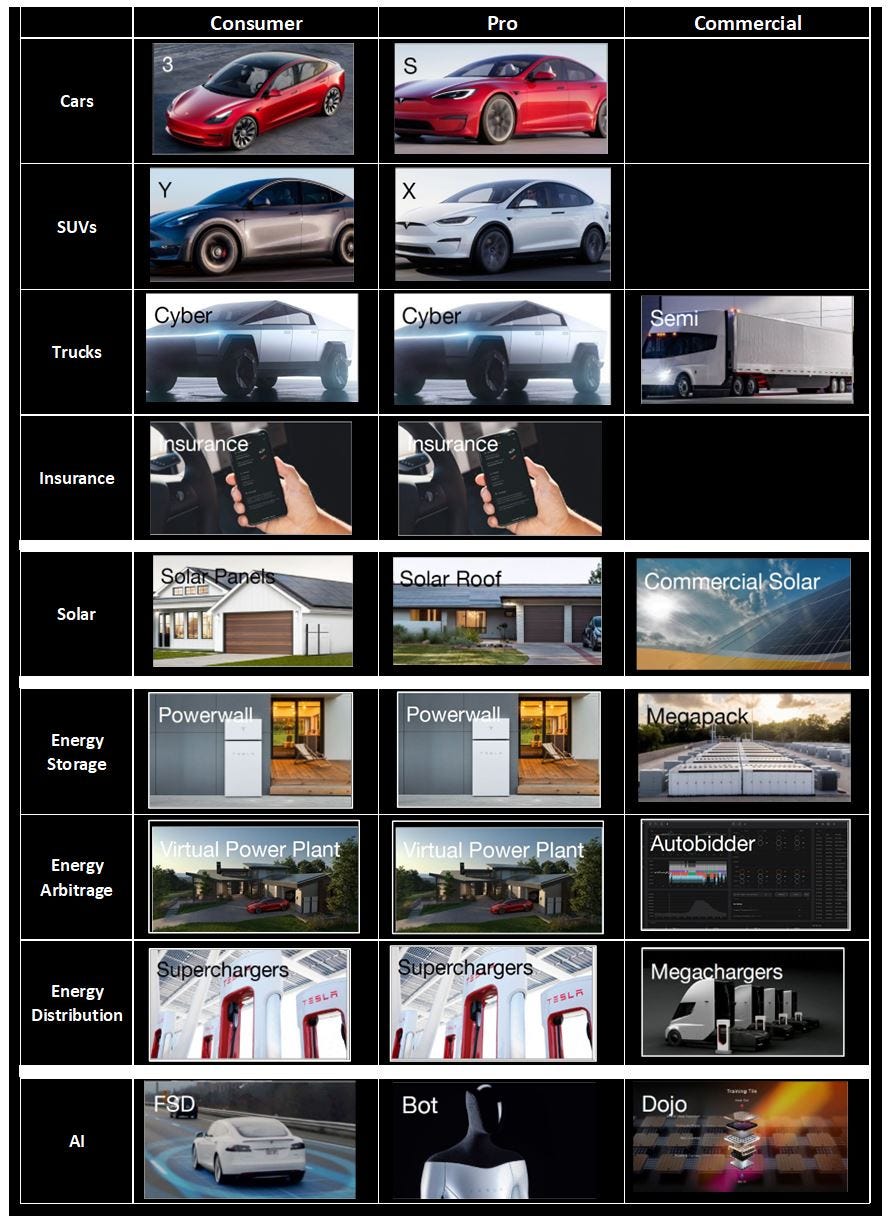

With respect to your main concern, the number of models, Tesla follows the same successful streamlined strategy as Apple (for reference, rated the highest investment-grade Aaa) does for Macs and iPhones, with a simple and clearly defined product matrix. Apple rakes in most of the profit in the phone market. Tesla does exactly the same in the EV car market, including refreshes of models to stay relevant, as the current S and X models .

Note the similarity between Tesla’s product mix compared to Steve Job’s mission matrix upon returning to Apple:

In contrast to car manufacturers that have a broad range of models, Tesla will not cannibalize sales of existing products. In your response at the Autopalooza 5, organized by Bloomberg on June 16, 2022, you praised Ford’s efforts to apply to their EV line the “streamlined Tesla approach” of fewer vehicles in key segments. After current OEMs spend what will be tens of billions of dollars in the hope of building enough EVs , what will they have accomplished ? They will have cannibalized their own existing sales with, essentially, no increase in revenue and no increase in profit. So zero ROI on tens of billions spent. For Tesla, every car sale is additional revenue and profit with very high margins. So what would you rather invest in ?

This year, sales of the Tesla Semi started and next year the CyberTruck will be delivered. You are of course aware that way more than 1 million reservation holders are more or less patiently waiting for their truck, right?From an investment point of view, would you rather invest in a company that has to cannibalize its own products or one that doesn’t? We have seen that Tesla reaches high sales numbers every time it enters a new car market. The electric Semi is going to be a game changer in the economics of transport by Semi, and the above mentioned gigantic number of preorders for the CyberTruck will take years to manufacture. So, just based on these two additional markets, how does the future of Tesla look from an investment point of view?

Tesla doesn’t need to fear the competition. It is way ahead when it comes to innovative manufacturing. An article in the Financial Times had already in November 2021 (now former) VW Chairman of the Management Board, Herbert Diess, complaining that Tesla can make a car in 10 hours, while it takes Volkswagen about 30.

While other car makers employ hundreds of robots to weld, screw, bolt and assemble the chassis together from hundreds of different parts (in Volkswagen’s case sourced from their over 40,000 suppliers), Tesla has made many robots redundant by using injection casting. This achieves a higher throughput with greater accuracy. Tesla pushes the envelope of vehicle manufacturing and safety by utilizing full-body injection molding for its vehicles; it’s latest acquisition of a CyberTruck mold is the largest of its kind ever created. When the low cost Tesla model comes, the body may well be made as a single piece. Meanwhile conventional manufacturers make platforms that have to serve many models, have to be developed years before they are put in usage, and are not optimally designed for any model.

Tesla has unparalleled demand for all their models in all countries in which they sell cars and is currently still production limited. With two new factories scaling up, there will soon be room to enter new markets or introduce models not previously sold into many countries. The recent sales of Model Y in Australia and New Zealand are examples of this.

In a recent poll graduates from MIT and Caltech were asked which company they want to work for: out of 30 companies, SpaceX and Tesla took the two top spots. Tesla’s greatest strength is the formidable and extraordinary teams of top engineers, scientists, physicists, software developer, AI specialists and manufacturers that Elon Musk has been assembling for over 15 years and which none of competing companies come close to. Is this taken into account in your qualitative evaluation ?

There is a big Tesla community, larger than for any other car brand. This in itself is another qualitative plus for Tesla. Arguments in this response also came from the Tesla community, who is avidly participating in our discussions.

Elon Musk is unique in that he participates too. With respect to the issue of investment grade his tweeted response was: Moody’s is irrelevant. If there ever was a moment in your life where you wanted to prove Mr. Musk wrong, this is that moment; but not the time to drag your feet if Moody’s wants to be ahead of the curve.

Thus, I hope that the above gives you a more well-rounded view on Tesla’s strategy and capabilities. Based on my professional view as a former Moody’s analyst, I believe that the qualitative view warrants the same conclusion as the quantitative view:

Tesla is investment grade and there is no qualitative ground to ding the rating to below investment grade. An upgrade is really overdue.

I remain at your full disposal should you wish to continue our discussions, by email or in person. And please do know, the world is watching.

Yours sincerely,

Alexandra Merz

During my two decades long banking career I have never read neither write so comprehensive and sharp and target oriented proposal as this one!!!

You’ve earned all of my personal and professional respect !!!

Excellent write up Alexandra and the Tesla community. Thanks so much! Interesting to see if Moodys can rise above their financial conflicts of interest and do the right thing