Tesla Is Overdue For Its Investment Grade Rating

Will This Lag Be Detrimental To The Rating Agencies?

Summary

Tesla Inc. is today still junk rated by both major rating agencies. For much longer?

All major debt related financial indicators prove that the upgrade to investment grade is overdue.

The impact of the upgrade to Investment Grade can be very consequential to the stock price.

Both rating agencies are under increased pressure to justify why they are delaying the overdue upgrade.

Investors even call on the SEC to oversee the blatant adjournment.

Credit Rating Agencies, are they still relevant?

Many investors still have today a bitter feeling towards the major rating agencies who failed them severely during the Global Financial Crisis, when many asset-backed securities and other bonds were critically overvalued.

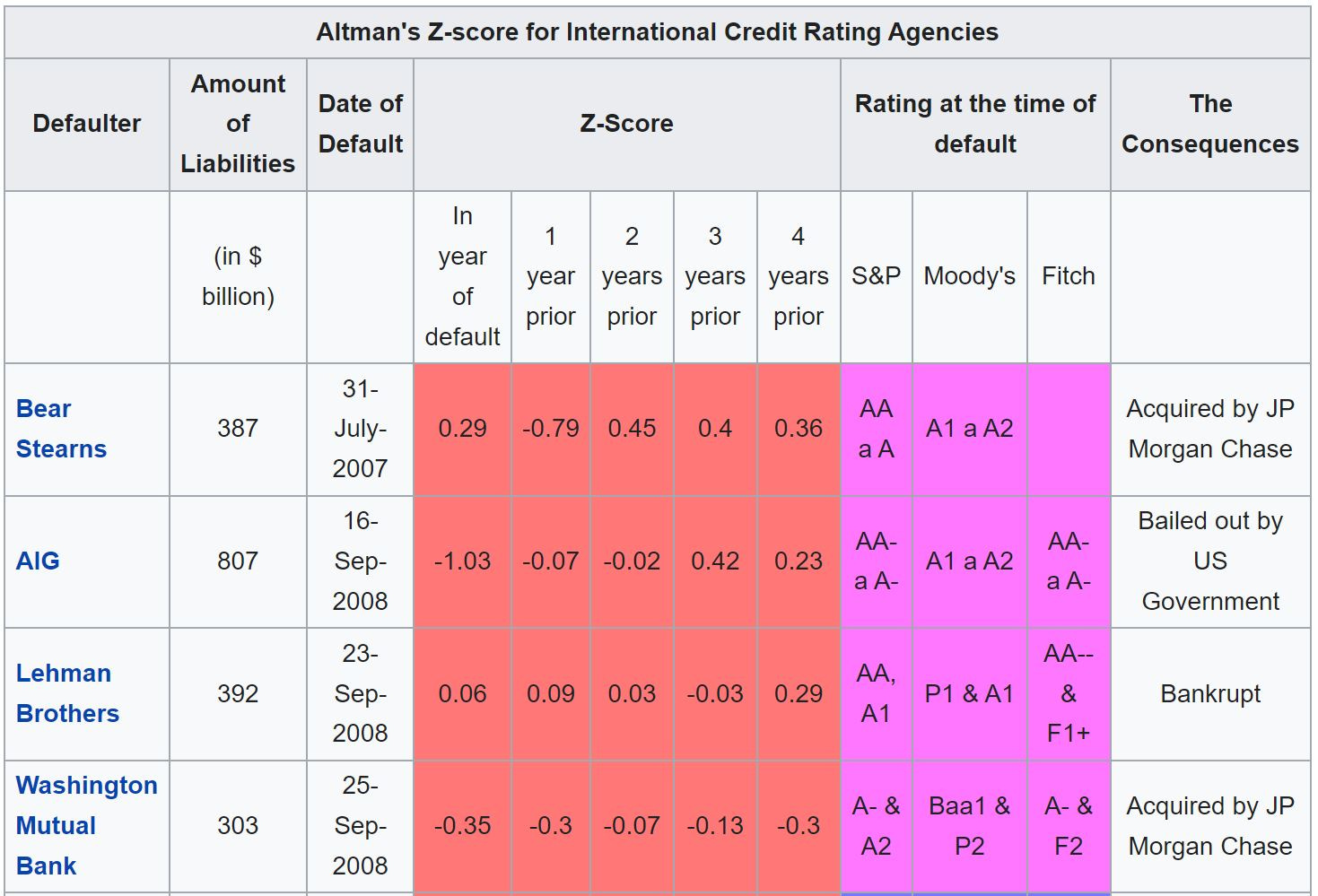

One early indicator for financial stress that is commonly used to detect suffering corporations is the Altman Z-score, a formula for predicting bankruptcy published in 1968 by Edward I. Altman, who was, at the time, an Assistant Professor of Finance at New York University. On the Wikipedia page dedicated to this indicator the following table shows how none of the rating agencies detected the financial stress on Bear Stearns, AIG, Lehman Brothers and Washington Mutual Bank - as none of the four companies lost their investment grade ratings despite having very low Altman Z-scores FOUR years prior to their default.

source: Wikipedia

Altman Z-Scores can be summarized to the following:

A score above 3 signals healthy financial conditions

A score between 1.1 and 3 signals the "grey zone"

A score below 1.1 signals the company is likely to face default in the two years to come.

For details on the calculations, please refer to Wikipedia.

Why does this matter for Tesla?

Tesla Inc's financials have improved steadily over the past quarters and have since Q4-2021 proven to be of Investment Grade. Yet, the rating agencies maintained the Speculative Grade (Junk) rating, avoiding comments on the matter.

https://www.jrw.com/articles/investment-principles/corporate-credit-ratings/ (JRW Investments)

Simultaneously, in May 2022, S&P ejected Tesla from the S&P 500 ESG index, pretexting stakeholder and media analysis which overruled the quantitative rating result. This was a clear sign for a heavy negative bias by the rating agency: to eject the most consequential company for environmental matters from the ESG index, while companies like Exxon and Chevron maintained their status within. For more background research on the matter, please refer to this video.

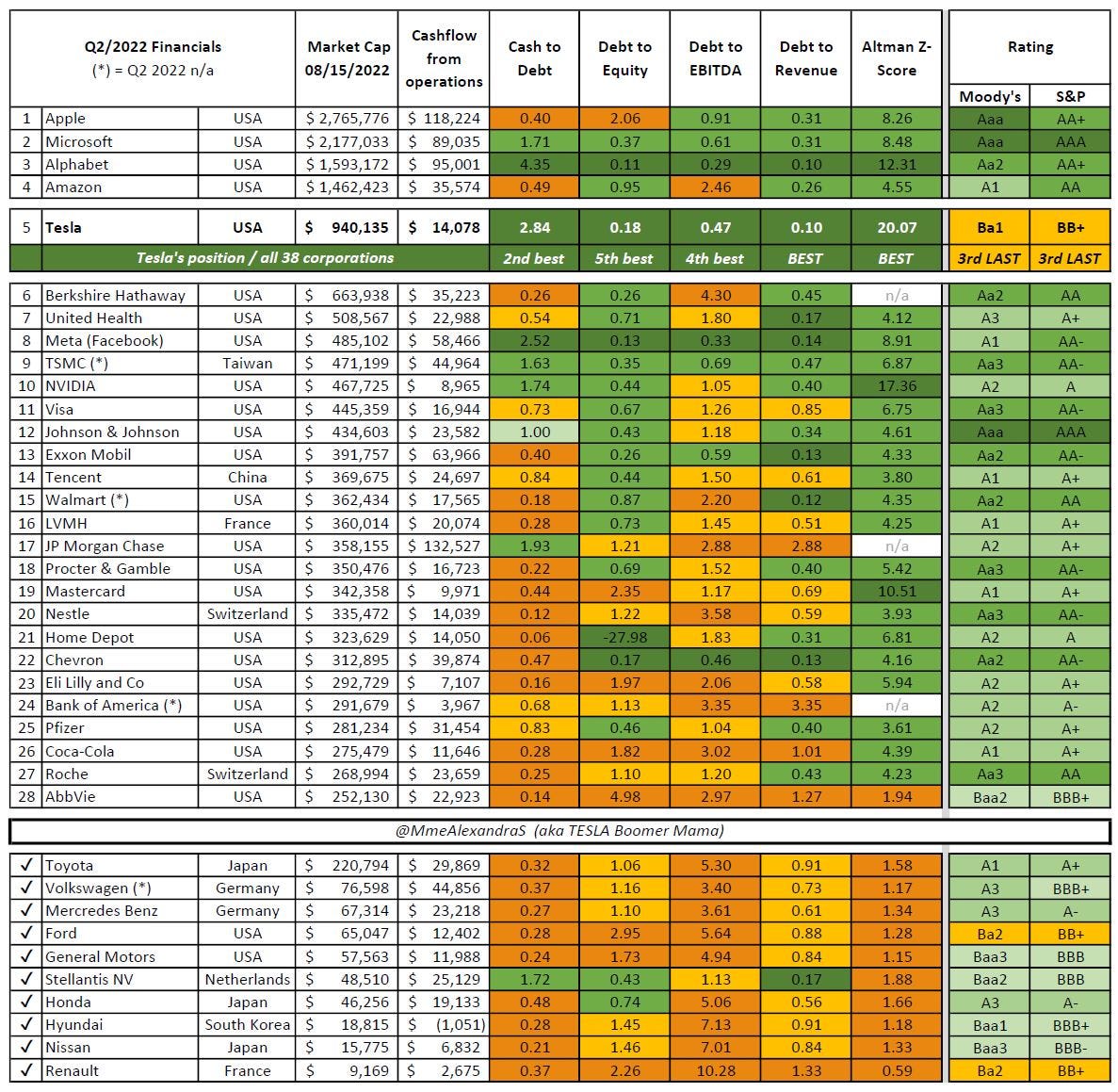

In February 2022, I started to assemble the following table, which was updated in May 2022 and again this week, on August 15, 2022. It shows the financial strength and creditworthiness, as well as the ratings, of Tesla and the other 27 biggest Mega Caps, as well as the ten biggest carmakers.

Tesla is today not only by far the most creditworthy carmaker (we can discuss at another moment whether it should still be considered a carmaker), AND among the three strongest Mega Cap companies worldwide. Yet, it is still rated "junk".

Let's look in detail at the results. Of the 38 corporations listed, Tesla:

is second best for its cash to debt ratio, meaning it would take them less than four months of cash flow from operations to reimburse all debt.

is in fifth place for the debt to equity ratio. Virtually no value of the company comes from its debt.

is fourth in class for its debt to EBITDA ratio, with a 0.48 very low ratio, signaling a very high probability the company can reimburse its debt easily.

is best for its debt to revenue ratio, with a 0.10 result, the same as Alphabet Inc. - best in class.

and LAST BUT NOT LEAST, TESLA is the best in class for the Altman Z- Score, with an outstanding 20.1 score:

What will happen when Tesla gets its investment grade rating?

Currently, institutional investors are hesitant to invest in Tesla. Some don't have a deep understanding of the disruptive nature of Tesla's EV business, leave alone the other branches of the corporation. Other reasons for the current reluctance include some overhang due to Elon Musk's interest in Twitter, a current high P/E ratio, concerns about possible EV competitors and uncertainty over future capital deployment.

All these concerns will be short lived. The Twitter overhang will be solved in two months, the capital deployment will be laid out with the announcement of future Giga factories (and followed eventually by buy-backs), the forward P/E ratios have rarely been so low (and will go lower in the near future, given the 50% annual growth rates of the company) and all competitors struggle to produce in mass and are yet to be seen throwing a shade on Tesla.

However, some funds are barred from investing in Tesla, purely by the current rating grade status. While it is difficult to quantify these investors, approximations suggest that $10tn of Assets under Management might be impacted by the future upgrade of Tesla to Investment Grade.

This upgrade, no matter to which level (and which most likely will happen in tiny steps, although I do believe a AA is warranted), will coincide with other major good news for the corporation, including the upcoming stock split at the end of this week, making the stock more affordable for investors and option purchasers.

And it may just start to fill the gap currently existing between the level of institutional ownership of Tesla compared to GM. When the pension funds, institutional investors and financial advisors who currently still operate with investment grade guidelines decide to allocate a mere 1% of their funds to $TSLA, the float will reduce significantly and new ATHs are possible in the weeks after the upgrade.

Data: GuruFocus

Whose reputation is really at stake?

The direction Tesla will ultimately take will be determined by the next chapter of the master plan laid out by Elon Musk, in his Master Plan Part Trois, detailing his grand vision for execution and investment, already set in motion by the previous two tomes (part 1 and part 2).

Tesla does not need rating agencies, as the company has barely any debt and could pay it off within weeks, if desired. However, institutional investors who are limited by antiquated guidelines to still use credit ratings, are depriving their clients from a generational stock and the evident stock price increase in the coming months and year.

This rating update is actually much more important to the rating agencies than to Tesla, who will execute its Master Plan, no matter a certain three letter combination (which proved far too often to be imprecise, late or blatantly wrong).

So now, I leave it to you, the investment community and the SEC to make your voices heard and ask Moody's Investor Services and S&P Global Ratings why they are still lagging with the overdue announcement. And to quote from Game of Thrones “Sooner would be better than later, and now would be better than sooner."

Excellent article and extremely on point! Painfully slow upgrades from both Moody's and S&P on Tesla's debt rating have the practical, real world effect of 'robbing' many State Teacher Retirement Funds, Pension Funds and Foundations from being able to participate in Tesla's robust growth. And that, in my humble opinion, is just plain wrong.

Excellent article, thanks for your efforts. It really makes one wonder which interests are at work behind the scenes to prevent Tesla from obtaining its more-than-justified investor status... The rating agencies were corrupt then and they are no doubt corrupt now..